January 22, 2019

London remains top gateway city in the world for commercial property investors

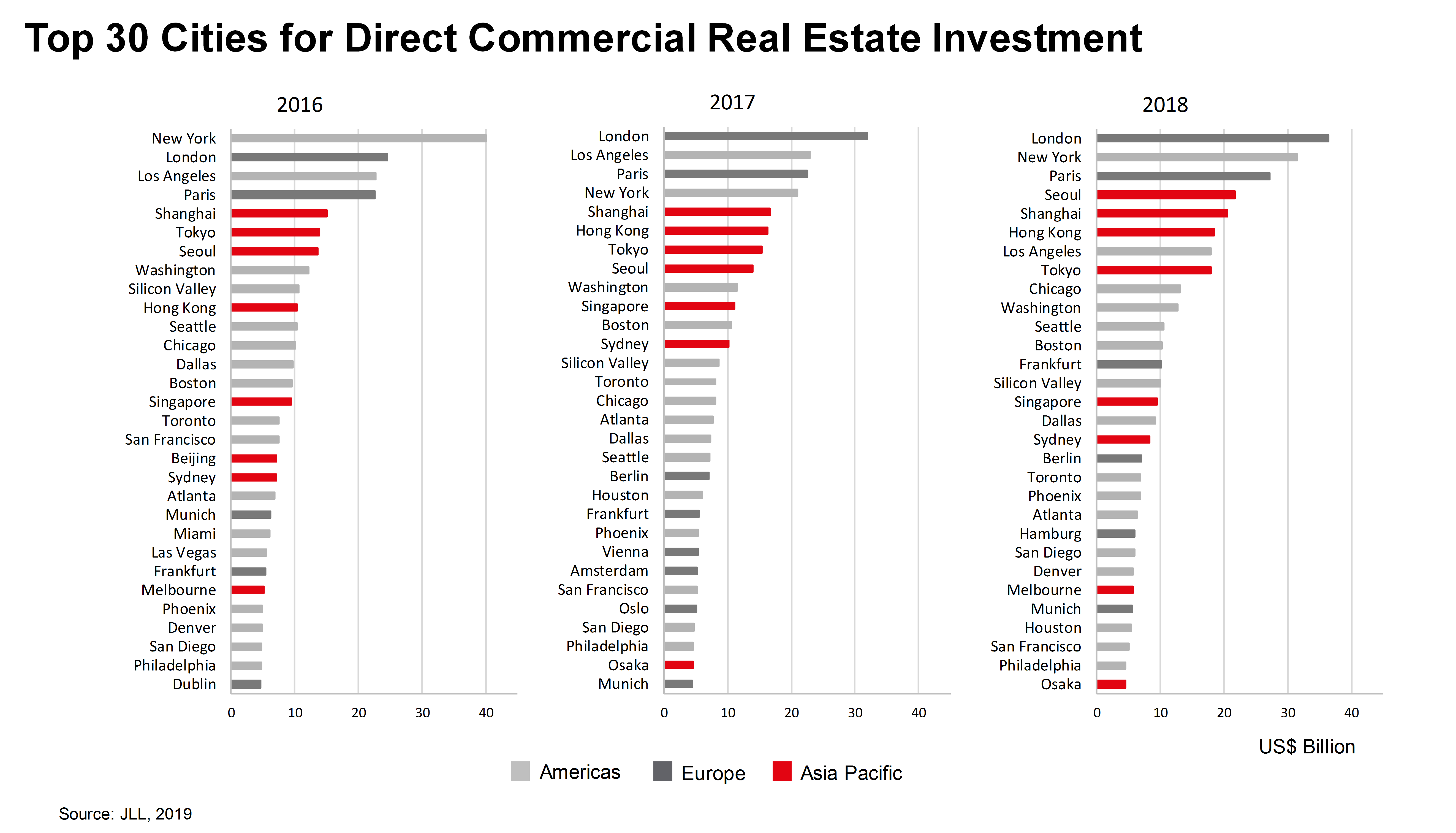

London maintained its position as the top city for global real estate investment in 2018, according to research published today by JLL. The report claims that investors continue to favour cities they are familiar with and that have well-established investment markets and high levels of transparency. Well-known, large gateway cities with the world’s deepest concentrations of capital, companies and talent continue to dominate the top ranks. Twelve cities–London, New York, Paris, Seoul, Hong Kong, Tokyo, Shanghai, Washington DC, Sydney, Singapore, Toronto and Munich–have appeared in the top 30 ranking every year for the past decade and account for 30 percent of all real estate investment.

London maintained its position as the top city for global real estate investment in 2018, according to research published today by JLL. The report claims that investors continue to favour cities they are familiar with and that have well-established investment markets and high levels of transparency. Well-known, large gateway cities with the world’s deepest concentrations of capital, companies and talent continue to dominate the top ranks. Twelve cities–London, New York, Paris, Seoul, Hong Kong, Tokyo, Shanghai, Washington DC, Sydney, Singapore, Toronto and Munich–have appeared in the top 30 ranking every year for the past decade and account for 30 percent of all real estate investment.

The data shows that total volumes in 2018 were $733 billion, up 4 percent from 2017, the best annual performance in a decade. Cross-border purchases accounted for 31 percent of activity in 2018, close to the 10-year average, suggesting investors still have appetite to buy outside their own markets.

Expectations for 2019

JLL projects that investment activity momentum will be maintained into 2019, as real estate continues to look attractive in comparison to other asset classes. Fundamentals in real estate remain compelling, despite historic low yields, as robust corporate occupier fundamentals across most markets are leading to positive returns. As such, investment activity may slow, but only marginally from its current high, as investors look to hold their real estate exposure and become more selective in the search for assets with strong income growth.

- The institutional real estate universe will continue to expand, driven by factors such as low volatility, diversification benefits, long-term income and an attractive pricing premium to core sectors. Asset classes such as student housing, senior living and multi-family have continued to attract more institutional money in 2018 and this is likely to continue in 2019.

- Industrial now accounts for 17 percent of all investment, up from 10 percent in 2009. In contrast, the retail sector has seen less activity as investors adjust their investment approach to reflect changing consumer behavior. In gateway cities, the office sector tends to account for a higher proportion of investment volumes—68 percent in 2018, compared to 51 percent in global volumes.

- The top 30 will continue to be dominated by the gateway cities in 2019. However, at the edges, investors will consider a widening range of cities in their strategies. Reflecting real estate investors’ risk appetite, secondary cities in established transparent markets, such as Osaka and Atlanta, are likely to attract more attention, as opposed to moving into entirely new countries.

Yields are now at historic lows in most markets across the globe. A sharp correction is unlikely, as there is still a significant weight of capital looking to invest in real estate, and corporate occupier market fundamentals across many markets are positive. This creates the potential for continued income growth. However, in 2019, overall investment volumes are expected to fall approximately 5 to 10 percent below the 2018 total, driven by a slightly reduced appetite from investors to sell, as well as continued selectivity in acquisitions.